It often starts pretty quietly—a simple email notification, maybe a message from your accountant, or, even worse, a formal letter straight from the Income Tax Department. For many people with jobs and small business owners, getting an income tax notice can feel less like a standard check-up and more like an unexpected deep dive into their entire financial life.

In India’s constantly changing world of finance and banking, tax scrutiny has definitely gotten more focused, more about the data, and increasingly automated. Tax notices aren’t rare surprises anymore; they’re part of a system that’s set up to keep an eye on financial activity across bank accounts, investments, and digital transactions. The key question isn’t just figuring out *why* these notices happen, but rather, how to steer clear of them from the very beginning.

The Shift: Why Income Tax Notices Are Rising

Over the last few years, things have quietly changed with India’s tax system. Tools like the AIS (Annual Information Statement) and TIS (Taxpayer Information Summary) mean the government now has a much clearer, almost real-time picture of your financial dealings.

Consider this: every big bank deposit, stock market trade, mutual fund purchase, credit card bill, or property you buy gets fed into a central system. Your financial history isn’t scattered anymore; it’s all linked up.

This change has really shifted what it means to be compliant in finance and banking. Before, small errors on your tax returns might have gone unnoticed. Now, any mismatches automatically trigger alerts.

And that’s often where those tax notices start – not usually because of deliberate fraud, but simply because something didn’t add up.

Where Most People Go Wrong

You know, it’s often not major tax evasion that triggers those income tax notices. More frequently, they pop up because of small mistakes that gradually add up.

Think about it: a salaried worker might simply forget to report the interest earned from their savings account. Or maybe a freelancer doesn’t report all their income, especially when it comes from several different gig platforms. An investor might even miss reporting the profit from selling some stocks.

These aren’t exactly huge, intentional tax frauds. They’re just everyday oversights that happen to people.

But here’s the thing: our tax system heavily relies on matching information. So, even tiny inconsistencies or mismatches can become glaringly obvious.

Smart Compliance: The Real Strategy

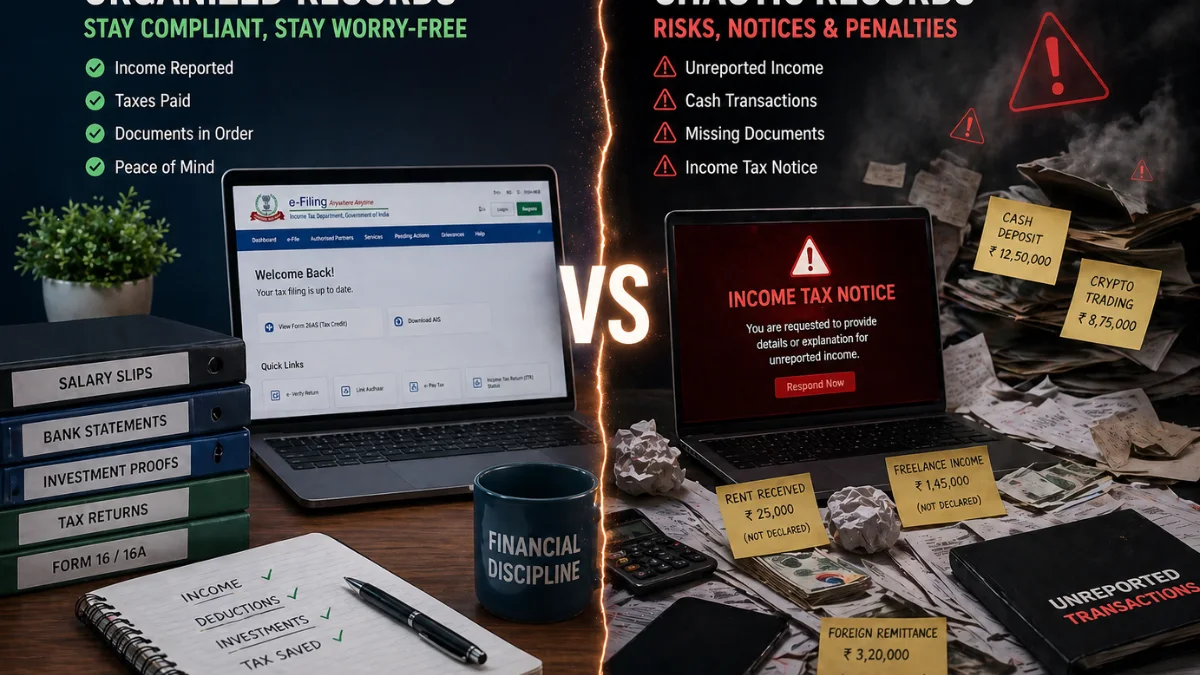

Avoiding an income tax notice isn’t about last-minute filing tricks. It’s about disciplined financial behavior throughout the year.

1. Align Your ITR with AIS and Form 26AS

Before filing your return, compare your declared income with AIS and Form 26AS.

These statements include:

- Salary income

- Interest earnings

- Dividend income

- Securities transactions

- High-value purchases

If your ITR doesn’t match these records, the system flags it.

The safest approach? Treat AIS as your baseline, not your afterthought.

2. Report All Sources of Income (Even the Small Ones)

One of the most common triggers for notices is unreported income.

This includes:

- Savings account interest

- Fixed deposit interest

- Freelance or side income

- Rental income

- Capital gains

In the Finance & Banking world, there’s a misconception that small amounts don’t matter. They do. Because the system already knows about them.

3. Avoid Cash Transactions That Don’t Add Up

Cash deposits, especially large ones, are closely monitored.

For example:

- Depositing ₹10 lakh or more in a savings account

- High cash transactions in business accounts

- Property purchases involving cash components

If your declared income doesn’t justify these transactions, it raises a red flag.

Digital transparency is now the norm. Cash opacity stands out.

4. Choose the Right ITR Form

It sounds basic, but choosing the wrong ITR form can lead to complications.

For instance:

- Using ITR-1 when you have capital gains

- Not declaring business income properly

- Misclassifying freelance income

The form you choose shapes how your income is interpreted. A mismatch here can invite unnecessary scrutiny.

5. Don’t Ignore High-Value Transactions

Banks and financial institutions report certain transactions directly to the tax department.

These include:

- Credit card bills above ₹1 lakh (cash) or ₹10 lakh (digital)

- Mutual fund investments

- Property transactions

- Foreign remittances

If these appear in AIS but not in your return, a notice is almost inevitable.

6. File Your Return on Time—Every Time

Late filing doesn’t just attract penalties. It increases your risk profile.

Regular, timely filing builds a consistent compliance record. Delays create gaps—and gaps invite questions.

In the broader Finance & Banking ecosystem, consistency is credibility.

The Psychology Behind Compliance

There’s a subtle behavioral pattern at play. Many taxpayers treat tax filing as a once-a-year task—something to “finish” rather than manage.

But compliance today is continuous.

Your financial behavior across the year—spending, investing, earning—feeds into a system that evaluates consistency. It’s less about catching fraud and more about identifying anomalies.

And anomalies often come from neglect, not intent.

What Happens If You Do Get a Notice?

Not all notices are alarming.

Some are:

- Informational (seeking clarification)

- Intimation notices (like Section 143(1))

- Scrutiny notices (more detailed review)

The key is not panic, but response.

A prompt, accurate reply—often with proper documentation—resolves most cases. Ignoring notices, however, escalates the issue.

The Business Angle: Why It Matters More Now

For professionals, freelancers, and small businesses, compliance isn’t just about avoiding penalties—it’s about financial credibility.

Banks assess tax returns before approving loans. Investors review compliance history. Even visa applications may involve financial scrutiny.

In that sense, clean tax records are part of your financial identity.

And in a digitized Finance & Banking environment, that identity is increasingly transparent.

The Future of Tax Monitoring in India

The direction is clear: deeper integration, smarter analytics, and reduced manual intervention.

Expect:

- Real-time data syncing between institutions

- AI-based risk profiling

- Pre-filled tax returns becoming more detailed

- Faster issuance of notices for discrepancies

In the near future, tax filing may feel less like reporting and more like verification.

The system will already know. You’ll just confirm.

More Read

Conclusion

Avoiding an income tax notice in India is no longer about being cautious at the time of filing. It’s about building a habit of financial clarity—where income, spending, and reporting align seamlessly.

The system has evolved. It sees more, connects faster, and questions sooner.

But it also rewards consistency.

Final Insight

In today’s Finance & Banking landscape, tax compliance isn’t a bureaucratic burden—it’s a reflection of financial discipline. The difference between a smooth filing experience and an unexpected notice often lies in small, everyday decisions. And those decisions, over time, define how transparent your financial life really is. STAY UPDATED STAY INFORMED –THE VUE TIMES

Frequently Asked Questions

What is the most common reason for income tax notices in India?

→ Mismatch between reported income and AIS/Form 26AS data is the most common trigger for notices.

Can I get a notice for small unreported income?

→ Yes, even small amounts like interest income can lead to notices if they appear in AIS but not in your return.

Is it safe to ignore an income tax notice?

→ No. Ignoring notices can escalate the issue and lead to penalties or legal action.

How can I check if my financial data matches tax records?

→ Review your AIS and Form 26AS before filing your ITR to ensure consistency.

Does late filing increase chances of getting a notice?

→ Yes, delayed filing can raise red flags and increase scrutiny from the tax department.