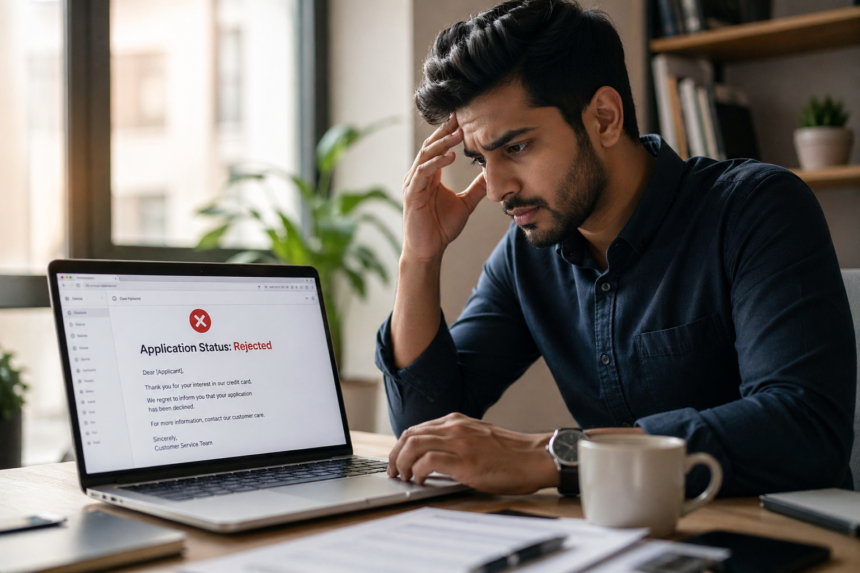

There’s a particular kind of silence that follows a rejected credit card application. No dramatic email. No clear explanation. Just a polite “We regret to inform you…” — and suddenly, your financial confidence takes a hit.

For many Indians stepping deeper into the world of Finance & Banking, a credit card isn’t just a payment tool. It’s a symbol. Of financial credibility. Of access. Of trust. And when that access is denied, the question lingers — what went wrong?

The truth is less mysterious than it feels, but more layered than most people realize.

The Invisible Filter in Finance & Banking

Banks don’t reject applications randomly. They follow a structured — and often unforgiving — evaluation system. Behind every “declined” status lies a mix of data points quietly working against you.

The most influential of these is your credit profile.

In India, this often means your CIBIL score. But here’s the nuance: it’s not just about having a score — it’s about the story behind it.

A score that’s too low signals risk.

No score at all signals uncertainty.

And in Finance & Banking, uncertainty is often treated as risk.

When “No Credit History” Becomes a Problem

It sounds counterintuitive. You’ve never taken a loan. Never defaulted. Never missed a payment. That should make you the ideal candidate, right?

Not quite.

Banks rely on past behavior to predict future reliability. Without a credit history, there’s nothing to evaluate. You’re essentially an unknown entity in the system.

This is why many first-time applicants — especially young professionals — face rejection.

From the bank’s perspective, approving you isn’t a calculated risk. It’s a blind one.

Income Isn’t Just About How Much You Earn

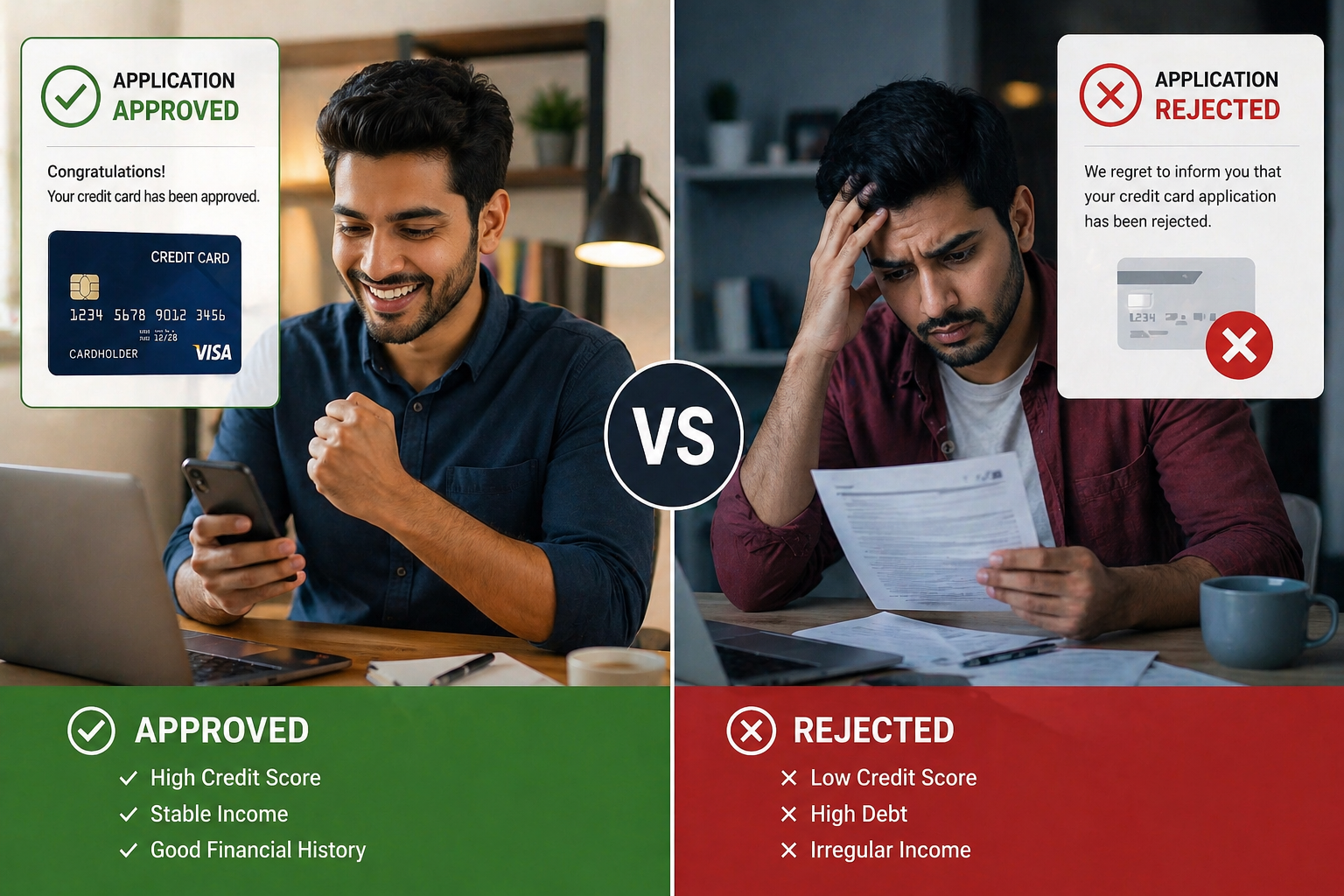

A common misconception is that a high salary guarantees approval. In reality, banks look beyond your income figure.

They evaluate stability. Consistency. Employer credibility.

A freelancer earning ₹1 lakh per month might still face rejection if income patterns are irregular. Meanwhile, someone earning ₹40,000 with a stable job at a recognized company could get approved more easily.

In Finance & Banking, predictability often outweighs potential.

The Debt Trap You Didn’t Notice

Another silent reason? Your existing financial obligations.

Banks calculate something called the debt-to-income ratio. If a large portion of your income is already committed to EMIs or loans, your ability to handle additional credit becomes questionable.

Even if you’ve never missed a payment, being over-leveraged sends a red flag.

It’s not about whether you’re paying.

It’s about how stretched you already are.

Too Many Applications, Too Little Time

This one surprises people.

Applying for multiple credit cards or loans within a short span can hurt your chances. Each application triggers a “hard inquiry” on your credit report. Too many of these signal desperation or financial stress.

Banks interpret this as risky behavior.

Ironically, trying harder to get approved can make approval less likely.

Errors You Didn’t Know Existed

Sometimes, rejection isn’t even your fault.

Incorrect details, mismatched addresses, outdated employment information — even minor discrepancies can trigger automated rejection systems.

In a system driven by data, small errors carry disproportionate consequences.

This is where the complexity of Finance & Banking systems becomes visible. It’s not just about your financial behavior — it’s about how accurately that behavior is recorded.

The Psychology Behind Rejections

There’s a subtle emotional layer to this process.

A rejected application often feels personal. But banks don’t evaluate you as a person — they evaluate patterns.

Still, the impact is real. People start questioning their financial decisions. Some avoid applying again. Others rush into risky alternatives like high-interest credit products.

Rejection doesn’t just affect your credit profile.

It reshapes your financial behavior.

Why This Matters More Today

Credit cards have evolved.

They’re no longer just about spending convenience. They offer cashback, travel perks, EMI options, and even serve as a gateway to building a financial identity.

In India’s rapidly digitizing economy — driven by UPI, fintech apps, and digital lending — access to credit is becoming a defining factor of financial inclusion.

Which means rejection isn’t just an inconvenience anymore.

It’s exclusion from a growing financial ecosystem.

What the Future of Finance & Banking Suggests

The system is slowly changing.

Alternative credit scoring models are emerging. Fintech platforms are using data like utility payments, rent history, and digital transactions to assess creditworthiness.

This shift could benefit millions who currently fall outside traditional evaluation systems.

But for now, the traditional rules still dominate.

And understanding them is the first step toward navigating them.

How to Improve Your Chances

There’s no shortcut, but there is a strategy.

Start small. A secured credit card or a small loan can help build your credit history.

Pay on time — every time. Even a single missed payment can leave a lasting mark.

Limit applications. Space them out.

Keep your financial profile clean and consistent.

In Finance & Banking, trust isn’t given instantly.

It’s built — transaction by transaction.

Conclusion

A rejected credit card application isn’t the end of your financial journey. It’s feedback — though often delivered without explanation.

The system may seem rigid, but it isn’t arbitrary. It rewards consistency, transparency, and patience.

Understanding why rejection happens shifts the narrative. From confusion to control. From frustration to strategy.

Because in the end, access to credit isn’t about luck.

It’s about alignment — between your financial behavior and the system evaluating it.

Final Insight

In a world where financial access increasingly defines opportunity, rejection is less about denial and more about readiness. The real advantage lies not in getting approved quickly — but in understanding the system deeply enough to never be rejected twice for the same reason.-THE VUE TIMES

Frequently Asked Questions

1. Why does my credit card application get rejected despite a good salary?

→ Banks evaluate more than income. Job stability, credit history, and existing liabilities play a major role in approval decisions.

2. What is the minimum CIBIL score required for a credit card?

→ Generally, a score above 750 is considered good, but some banks may approve cards for lower scores depending on other factors.

3. Can I apply again after rejection?

→ Yes, but it’s advisable to wait at least 3–6 months and improve your financial profile before reapplying.

4. Does applying multiple times affect my credit score?

→ Yes, multiple applications trigger hard inquiries, which can temporarily reduce your credit score and signal risk to banks.

5. How can I build credit if I have no history?

→ Start with a secured credit card or small loan, and ensure timely repayments to gradually build a positive credit profile.