You know that surprising moment when things seem perfect, but then something goes wrong? You apply for a loan—a car loan, maybe, or a mortgage—and you feel totally prepared. You’ve got a stable job, some savings, and a clean financial history. Then, the bank either says no, or, even worse, says yes but with an interest rate that makes you cringe.

That moment usually comes down to one quiet factor: your credit score.

In India’s ever-changing world of finance and banking, your credit score has quietly turned into a key part of your financial identity. It’s not just about loans anymore. It affects how much banks trust you, how fast they approve your applications, and even how much your financial choices end up costing you.

And the frustrating thing? Many people don’t realize how easily their score can drop, or how they can smartly work to improve it.

Why Credit Scores Matter More Than Ever in Finance & Banking

Here in India, when people talk about credit scores, they’re often thinking about the big names like CIBIL, Experian, or Equifax. These scores usually run from 300 to 900. Generally, if you’re above 750, that’s seen as a solid score. Go below that, and lenders might start seeing you as a bit more of a risk.

But what’s really changing isn’t just the score number itself. It’s how hard banks are pushing it into their processes these days.

With digital loans, instant approvals, and all those fintech apps making borrowing easier than ever, things have also become much more automated. Decisions are made faster, involve less human judgment, and really focus on your past financial behavior.

Basically, your credit history is often speaking much louder than your current income.”

The Real Reasons Credit Scores Drop (Even When You Think You’re Careful)

A lot of people think poor credit usually comes from something huge, like a major default. But that’s not usually what happens.

More often than not, it’s the result of small, repeated habits over time:

* Things like being a few days late on a credit card payment.

* Regularly using almost 90% of your available credit.

* Applying for several loans all at once, in a short span.

* Leaving old, unpaid bills unresolved.

These things might not feel like “big mistakes” to you, but in the eyes of the finance and banking world, they act as red flags, suggesting instability.

Try thinking of your credit score as more like a report on your financial habits and behavior, rather than just a number reflecting your finances.

How to Improve Your Credit Score Fast in India

Speed matters when you’re preparing for a loan or financial milestone. While credit repair isn’t instant, certain actions can create noticeable improvement within a few months.

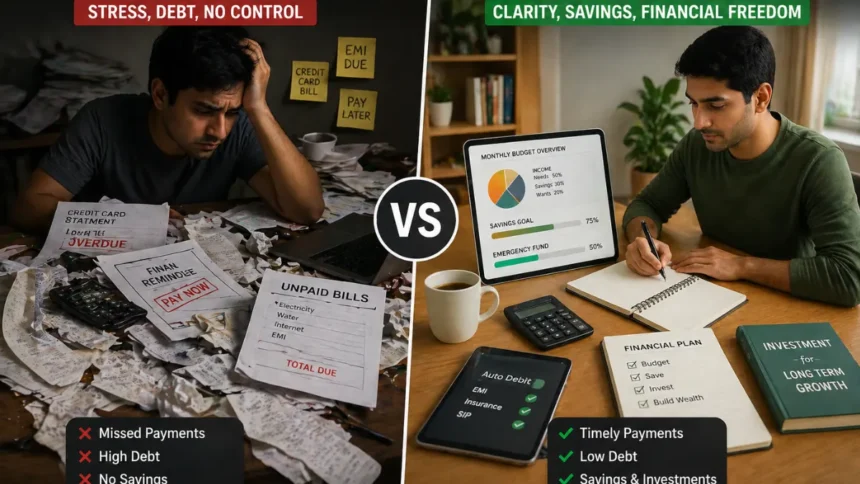

1. Pay All Dues — Not Just Minimums

Paying the minimum amount on your credit card keeps you compliant, but not healthy.

Banks prefer borrowers who clear full dues consistently. Even one delayed payment can drop your score significantly. Clearing outstanding balances quickly is the fastest way to rebuild trust in Finance & Banking records.

2. Reduce Your Credit Utilization Ratio

This is one of the most overlooked factors.

If your credit limit is ₹1 lakh and you regularly use ₹80,000, your utilization is 80%. Ideally, it should stay below 30%.

High usage suggests dependency. Lower usage signals control.

A simple trick? Either reduce spending temporarily or request a higher credit limit without increasing your actual expenses.

3. Avoid Multiple Loan Applications

Every time you apply for credit, lenders perform a “hard inquiry.” Too many of these in a short period creates the impression that you’re desperate for credit.

In the Finance & Banking ecosystem, this is a red flag.

Be selective. Apply only when necessary — and preferably after improving your score slightly.

4. Keep Old Credit Accounts Active

Length of credit history matters.

Many people close old credit cards thinking it’s responsible behavior. In reality, older accounts strengthen your profile by showing long-term reliability.

An old, well-managed account is one of your biggest assets in building a strong credit score.

5. Fix Errors in Your Credit Report

This is where things get surprisingly unfair.

Sometimes, your score drops due to errors — incorrect defaults, duplicate entries, or unresolved loans that you’ve already cleared.

You can check your report via official portals and raise disputes with agencies like CIBIL.

Corrections can boost your score faster than behavioral changes.

6. Use a Secured Credit Card (If Needed)

If your score is very low or you have no credit history, banks may hesitate.

A secured credit card — backed by a fixed deposit — can help rebuild your profile. It reduces risk for the lender while giving you a chance to demonstrate discipline.

It’s a slow start, but often the most reliable one.

The Psychology Behind Credit Behavior

What’s fascinating is how closely credit scores mirror human behavior.

Impulse spending, delayed payments, financial stress — they all show up in your score.

In India, where credit culture is still evolving, many people treat loans emotionally rather than strategically. But the Finance & Banking system doesn’t interpret emotions — it reads patterns.

That’s why improving your credit score isn’t just about numbers. It’s about building predictable, disciplined financial habits.

Why This Topic Is Trending in India

The surge in personal loans, BNPL (Buy Now Pay Later) options, and digital credit apps has brought credit scores into mainstream awareness.

Younger professionals, freelancers, and even students are entering the credit ecosystem earlier than ever.

At the same time, rising interest rates and stricter lending norms mean banks are becoming more selective.

This combination — easy access but stricter evaluation — is why improving your credit score fast has become a priority conversation in Finance & Banking today.

What the Future Looks Like

Credit scoring in India is evolving beyond traditional models.

Alternative data — like utility bill payments, rent history, and digital transaction behavior — is starting to influence lending decisions.

Fintech platforms are experimenting with more inclusive scoring systems, but traditional scores still dominate.

What’s clear is this: your financial reputation will become even more data-driven.

And those who understand the system early will have a significant advantage.

More Read

Conclusion

Improving your credit score isn’t about gaming the system — it’s about aligning with how the system works.

Small, consistent actions create long-term credibility. Quick fixes exist, but they only work when backed by disciplined habits.

In the broader landscape of Finance & Banking, your credit score is less of a judgment and more of a reflection.

And reflections, unlike opinions, can be changed — but only through consistent action.

Final Insight

At its core, a credit score is not just a number assigned by banks — it’s a quiet narrative of your financial decisions. In a world where access to money is becoming faster but trust is becoming stricter, those who understand this narrative will move ahead, not just financially, but strategically. That’s where the real power lies.-The Vue Times

Frequently Asked Questions

1. How long does it take to improve a credit score in India?

It usually takes 3–6 months to see noticeable improvement, depending on your actions like clearing dues and reducing credit usage.

2. What is a good credit score in India?

A score above 750 is generally considered good and improves your chances of loan approval with better interest rates.

3. Can paying off loans increase my credit score immediately?

It helps, but not instantly. The impact reflects after the next reporting cycle, usually within 30–45 days.

4. Does checking my credit score reduce it?

No, checking your own score is a “soft inquiry” and does not affect your credit score.

5. Can I get a loan with a low credit score?

Yes, but with higher interest rates or stricter conditions. Improving your score first is always better.