It usually begins quietly. A late-night scroll, a financial crunch, a notification promising “instant approval” with no paperwork. Within minutes, money lands in a bank account. Relief follows—briefly.

Then the calls start.

At first, polite reminders. Then aggressive warnings. Soon, messages arrive not just on your phone, but on your contacts’ phones—friends, colleagues, even distant relatives. Screenshots, threats, humiliation tactics. The loan that looked like a quick fix begins to feel like a trap that knows too much.

This isn’t an isolated story anymore. Across India, digital loan apps have become a growing concern, raising serious questions about Cybersecurity & Safety in the age of instant finance.

The Illusion of Instant Credit

The surge in popularity of loan apps in India is deeply connected to the country’s rapid digital growth. The widespread availability of affordable data, the increasing ownership of smartphones, and a large population that traditional banks haven’t fully served have all combined to create a fertile ground for financial technology breakthroughs. Many genuine platforms have genuinely made it easier for people to borrow money.

However, alongside these legitimate services, a troubling underground network has also appeared. These apps might look like regular financial services, but they often operate with very little oversight or responsibility.

These apps often lure users with promises of quick and easy loans. They claim you can get money fast without credit checks or lengthy applications—just download the app, grant a few permissions, and the funds could be available within hours. When someone is dealing with immediate financial needs, like unexpected medical bills, rent payments, or simply trying to make ends meet day-to-day, such offers can be incredibly hard to resist.

But what isn’t immediately clear is the hidden cost that comes with this convenience.

Where Cybersecurity & Safety Begin to Break Down

You know, a lot of these apps don’t just want basic info; they’re asking for deep access to your phone.

They want your contacts, your photos, your messages, your call history, even your location.

For most people, these requests don’t seem like a big deal because so many apps ask for similar permissions. But when it comes to those unregulated loan platforms, handing over this data is like giving them leverage.

Once you grant that access, you’re basically letting them hold your digital identity. And things can turn sour fast if you run into trouble repaying the loan—maybe because the terms were confusing or the interest was sky-high. That’s when the harassment starts.

They dig through your contacts, they might misuse your photos, they turn your personal information into a weapon.

That’s when worrying about cybersecurity and safety stops being just about tech stuff and becomes a deeply personal concern.

The Business Model Behind the Threat

It’s tempting to dismiss these as just random cons, but that’s not really the case. In fact, many of them work on a very deliberate strategy.

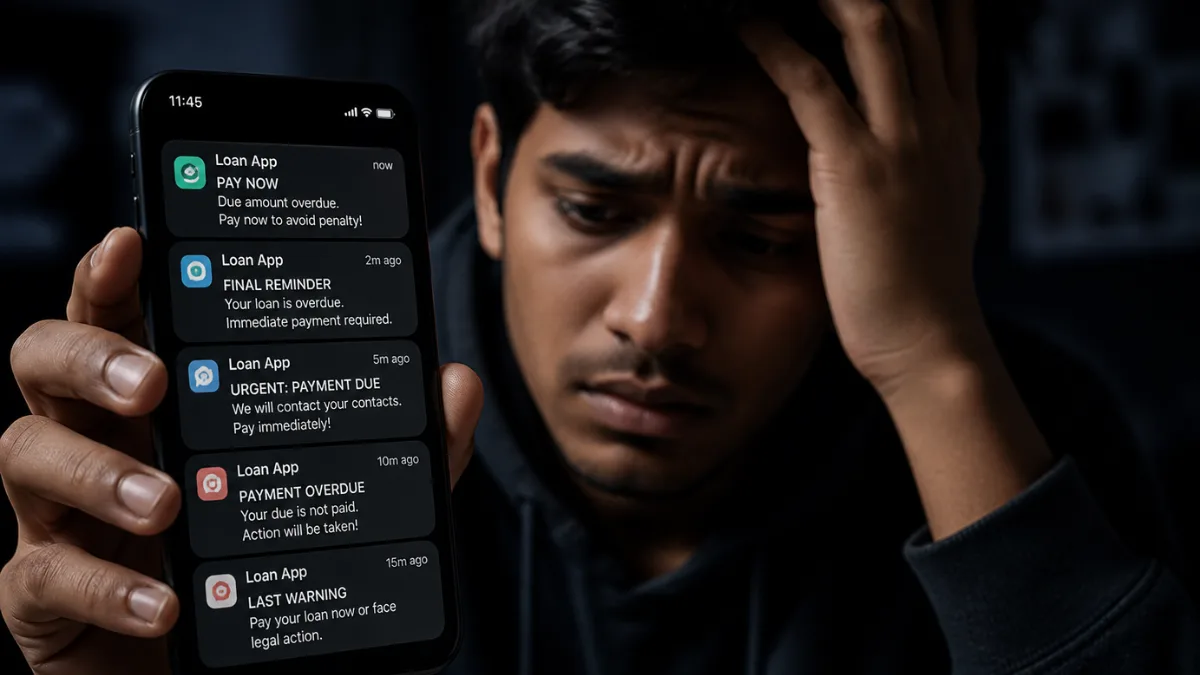

Short repayment periods—sometimes as short as a week—paired with hefty fees are designed to make it tough for borrowers to stay on track. And if they miss a payment, the fines pile up fast.

But the main money isn’t just from getting repaid. It’s all about the pressure they put on people.

Making borrowers feel ashamed is now part of the game. People talk about receiving altered photos sent to their friends and family, messages that accuse them of cheating, and endless calls meant to scare them. The aim is straightforward: scare them into paying up.

This isn’t just bad behavior—it’s a widespread misuse of our digital systems.

Why It’s Becoming a National Concern

India has already seen regulatory action in this space. Authorities have flagged hundreds of suspicious apps, and app stores have removed many of them. Yet, new ones keep appearing.

The reason is simple: demand.

A large segment of the population still lacks access to formal credit. Traditional banks require documentation, credit history, and time. Loan apps exploit this gap, offering speed where institutions offer caution.

At the same time, digital literacy hasn’t kept pace with digital access. Users know how to download apps—but not always how to evaluate them.

This gap is where Cybersecurity & Safety risks multiply.

The Psychology of Digital Pressure

What makes these apps particularly dangerous isn’t just the data access—it’s how that data is used.

Financial stress already puts users in a vulnerable state. Add social pressure, and the impact intensifies. The fear of public embarrassment often outweighs rational decision-making.

Borrowers don’t just repay loans—they scramble to protect their reputation.

In some reported cases, individuals have taken extreme steps under this pressure. It’s a stark reminder that digital threats aren’t confined to screens. They spill into real lives, real relationships, and real consequences.

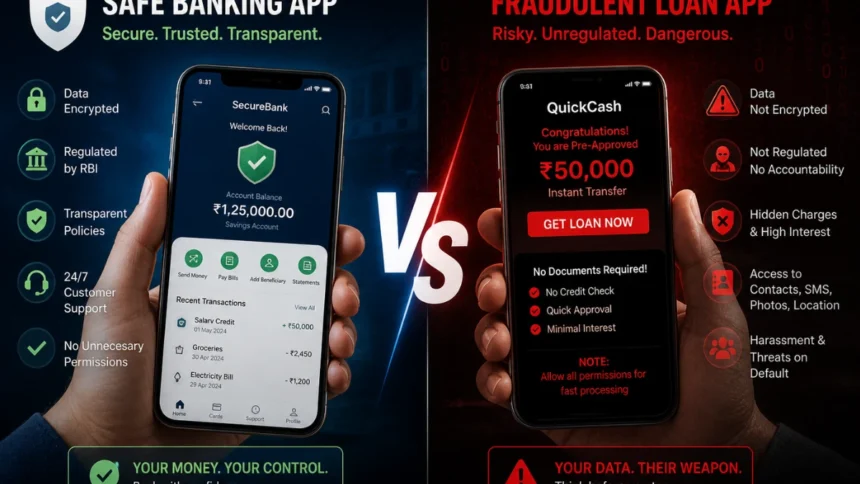

How to Stay Safe: Practical Cybersecurity & Safety Measures

Avoiding these traps doesn’t require technical expertise. It requires awareness and caution.

Start with the basics. Not every app deserves your trust.

1. Verify Before You Install

Check if the app is registered with financial authorities. Look for clear company details, a verifiable website, and transparent policies. If information feels vague, it probably is.

2. Question Permissions

Why does a loan app need access to your contacts or gallery? In most cases, it doesn’t. Deny unnecessary permissions and reconsider using apps that insist on them.

3. Read the Fine Print

Interest rates, processing fees, repayment timelines—these details are often buried. A loan that looks small upfront can grow quickly due to hidden charges.

4. Stick to Trusted Platforms

Use apps from established banks or recognized financial institutions. They may take longer, but they operate within regulatory frameworks.

5. Protect Your Data

Avoid sharing sensitive documents casually. Once uploaded, control is lost. Treat your digital identity like you would your physical documents.

6. Report Suspicious Activity

If you encounter harassment or suspect fraud, report it to cybercrime portals or local authorities. Silence allows these systems to continue.

The Future of Digital Lending and Cybersecurity & Safety

The digital lending space isn’t going away. If anything, it’s expanding.

Regulation will likely tighten. App stores may introduce stricter checks. Financial literacy campaigns could improve awareness. But technology evolves quickly, and so do the methods used by bad actors.

The responsibility, at least for now, is shared.

Platforms must build ethical systems. Regulators must enforce boundaries. But users must also recognize that convenience often comes with hidden risks.

The next phase of Cybersecurity & Safety won’t just be about protecting devices. It will be about protecting dignity, privacy, and financial stability in an increasingly connected world.

More Read

Conclusion

Loan apps are not inherently dangerous. But the ecosystem they exist in can be.

The difference between a legitimate financial tool and a predatory system often comes down to transparency, regulation, and intent. Unfortunately, not all apps meet that standard.

What makes this issue urgent isn’t just the financial risk—it’s the human cost. Privacy violations, emotional distress, and reputational damage aren’t abstract threats. They are lived experiences for many users.

Digital finance promised empowerment. In some cases, it has delivered exploitation instead.

Final Insight

At The Vue Times, the focus isn’t just on trends—it’s on the systems shaping everyday decisions. Loan apps are a reminder that not all innovation moves in the right direction. As digital tools become more powerful, the line between convenience and control becomes thinner.-The Vue Times

Staying informed isn’t optional anymore. It’s a form of protection.

Frequently Asked Questions

1. Are all loan apps unsafe?

No, many legitimate loan apps are operated by banks and regulated institutions. The risk comes from unverified or illegal apps that misuse user data and apply unethical practices.

2. Why do loan apps ask for contact permissions?

Legitimate apps usually don’t require access to contacts. Fraudulent apps use this data to threaten or harass users during repayment disputes.

3. What should I do if I’m being harassed by a loan app?

Document all communications and report the issue to India’s cybercrime portal or local police. Avoid engaging directly with threats.

4. How can I identify a fake loan app?

Look for missing company details, unrealistic promises, poor reviews, and excessive permission requests. These are common warning signs.

5. Is it safe to upload personal documents on loan apps?

Only if the app is verified and regulated. Otherwise, your documents could be misused for fraud or identity theft.