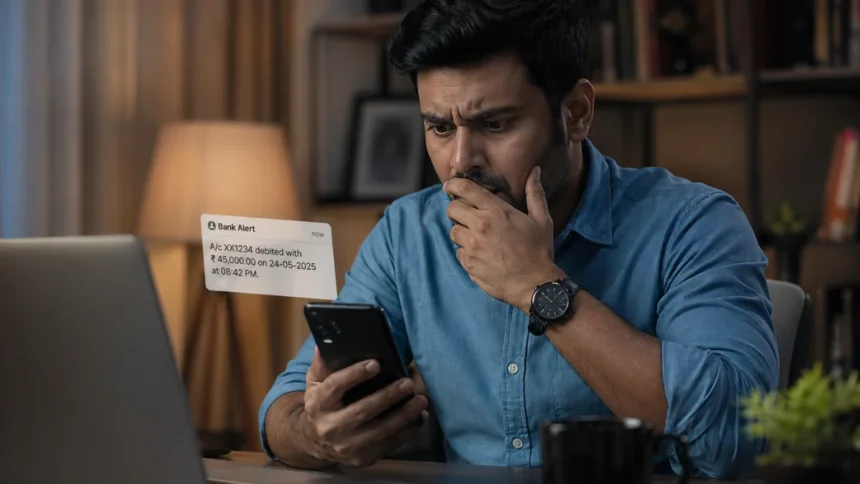

There’s a specific kind of panic that doesn’t come from loud alarms or dramatic events—it arrives quietly, often in the form of a notification. A debit alert you don’t recognize. A login you didn’t initiate. A balance that suddenly looks unfamiliar.

For many people, the realization doesn’t hit immediately. It lingers for a few seconds—maybe this is a mistake?—before turning into a sharper question: What just happened to my money?

This is where Cybersecurity & Safety stops being an abstract concept and becomes intensely personal.

When Digital Trust Breaks

Banking today runs on invisible systems—UPI transfers, net banking, auto-debits, mobile apps. These tools have made life faster, smoother, and far more convenient. But they’ve also shifted trust from physical counters to digital interfaces.

And when something goes wrong, the absence of a human intermediary makes the experience feel even more unsettling.

Cyber fraud in India and globally has seen a noticeable rise—not because systems are weak, but because attackers have become smarter. Phishing messages now mimic real banks. Fake apps look identical to official ones. Even calls can sound convincing enough to trick careful users.

The question is no longer if cyber threats exist. It’s how prepared you are when one finds its way to you.

The First Few Minutes Matter More Than You Think

The biggest mistake people make after discovering a hacked bank account isn’t ignorance—it’s hesitation.

Those first 10–15 minutes can determine whether the damage stops or spreads.

Start with the obvious but critical step: immediately contact your bank. Most banks offer 24/7 helplines and emergency blocking options. Freeze your account or card access. Don’t wait to “confirm” the fraud further—assume it’s real and act.

If your account is linked to UPI or mobile apps, disable those temporarily. Change your passwords—not just for banking, but also for email and other linked services.

Because here’s the uncomfortable truth: if one entry point is compromised, others might be at risk too.

Cybersecurity & Safety: Reporting Isn’t Optional

A common hesitation is whether to file a complaint. Many assume small losses aren’t worth the effort. But reporting is not just about recovery—it’s about accountability.

In India, cyber fraud complaints can be registered through the national cybercrime portal or helpline (1930). Timing plays a crucial role. The faster you report, the higher the chances that the transaction can be traced or even reversed.

Banks and authorities now collaborate more closely than before. There are mechanisms designed to flag suspicious transfers and freeze beneficiary accounts. But these systems depend heavily on quick reporting.

Delay turns recoverable fraud into permanent loss.

Understanding How It Happened

Once immediate damage control is in place, the next step is uncomfortable but necessary—figuring out how the breach occurred.

Was it a phishing link? A suspicious app download? Sharing OTP unknowingly? Using public Wi-Fi for banking?

Most hacks don’t come from sophisticated “Hollywood-style” cyber attacks. They come from small, everyday vulnerabilities.

Someone clicks a link that looks like a courier update. Another installs an app that promises cashback. A third shares banking details during a call that “sounds official.”

Cybersecurity isn’t just about systems—it’s about behavior.

And that’s where the deeper challenge lies.

The Psychology Behind Cyber Frauds

Cybercriminals don’t just hack systems—they study people.

Urgency is their favorite tool. “Your account will be blocked.”

Authority is another. “This is your bank calling.”

Fear, curiosity, and even greed often play a role.

The attacks succeed not because users are careless, but because the situations are engineered to override caution.

Understanding this psychological layer is essential for long-term Cybersecurity & Safety. It shifts the focus from blaming users to recognizing patterns.

Because once you see the pattern, it becomes harder to fall for it again.

Financial Impact Is Only One Part of the Damage

Losing money is the most visible consequence. But it’s rarely the only one.

There’s a lingering anxiety that follows—checking your account repeatedly, second-guessing every notification, questioning every digital interaction.

Trust, once broken, doesn’t rebuild instantly.

For businesses, the stakes are even higher. A compromised account can disrupt operations, damage reputation, and lead to legal complications.

This is why cybersecurity is no longer just an IT issue. It’s a financial and psychological one.

Cybersecurity & Safety in a Digital Economy

India’s rapid digital adoption—UPI growth, mobile banking, fintech expansion—has created one of the most advanced digital payment ecosystems in the world.

But scale brings exposure.

More users mean more entry points. More transactions mean more opportunities for fraud.

The challenge isn’t to slow down digital growth—it’s to strengthen the safety net around it.

Banks are improving fraud detection systems. Governments are pushing awareness campaigns. But individual vigilance remains the first line of defense.

What You Should Do Next (After Immediate Action)

Once the immediate threat is handled, don’t move on too quickly.

Review your bank statements thoroughly. Look for smaller unauthorized transactions—sometimes attackers test with small amounts before larger withdrawals.

Enable transaction alerts if they weren’t already active. Consider setting daily transaction limits. Update your KYC details if needed.

Also, reinstall official banking apps from verified sources. Avoid using third-party apps for financial access unless absolutely necessary.

This isn’t paranoia—it’s recalibration.

The Future of Cybersecurity & Safety

As banking becomes more digital, cybersecurity will become more invisible—but also more integrated.

Biometric authentication, AI-based fraud detection, behavioral analytics—these tools are already shaping the next phase of financial security.

But technology alone won’t solve everything.

The real shift will come from awareness becoming habit. When people instinctively question suspicious messages. When sharing OTP feels as risky as handing over cash. When digital literacy becomes as essential as financial literacy.

That’s when cybersecurity stops being reactive and becomes preventive.

More Read

Conclusion

A hacked bank account is no longer an unusual event—it’s a growing reality of a connected world. The difference lies not in whether you face it, but in how you respond.

Speed, awareness, and action define the outcome.

And perhaps the most important lesson is this: security is not a one-time setup. It’s an ongoing practice.

Final Insight

Digital convenience has made money feel frictionless—but that same ease demands sharper awareness. In a world where transactions happen in seconds, trust must move just as fast. Cybersecurity & Safety is no longer a technical concern—it’s a personal responsibility. Stay Updated Stay Informed-The Vue Times

Frequently Asked Questions

1. What should I do immediately if my bank account is hacked?

→ Contact your bank instantly to block your account or card. Change all passwords and report the fraud through official cybercrime channels.

2. Can I recover money lost due to cyber fraud?

→ Yes, if reported quickly. Authorities may freeze the transaction trail, increasing chances of recovery depending on timing.

3. How do hackers usually access bank accounts?

→ Common methods include phishing links, fake apps, OTP scams, and compromised devices or networks.

4. Is it safe to use public Wi-Fi for banking?

→ No. Public Wi-Fi networks are often unsecured and can expose sensitive data to attackers.

5. How can I improve my Cybersecurity & Safety?

→ Use strong passwords, enable two-factor authentication, avoid suspicious links, and regularly monitor your account activity.