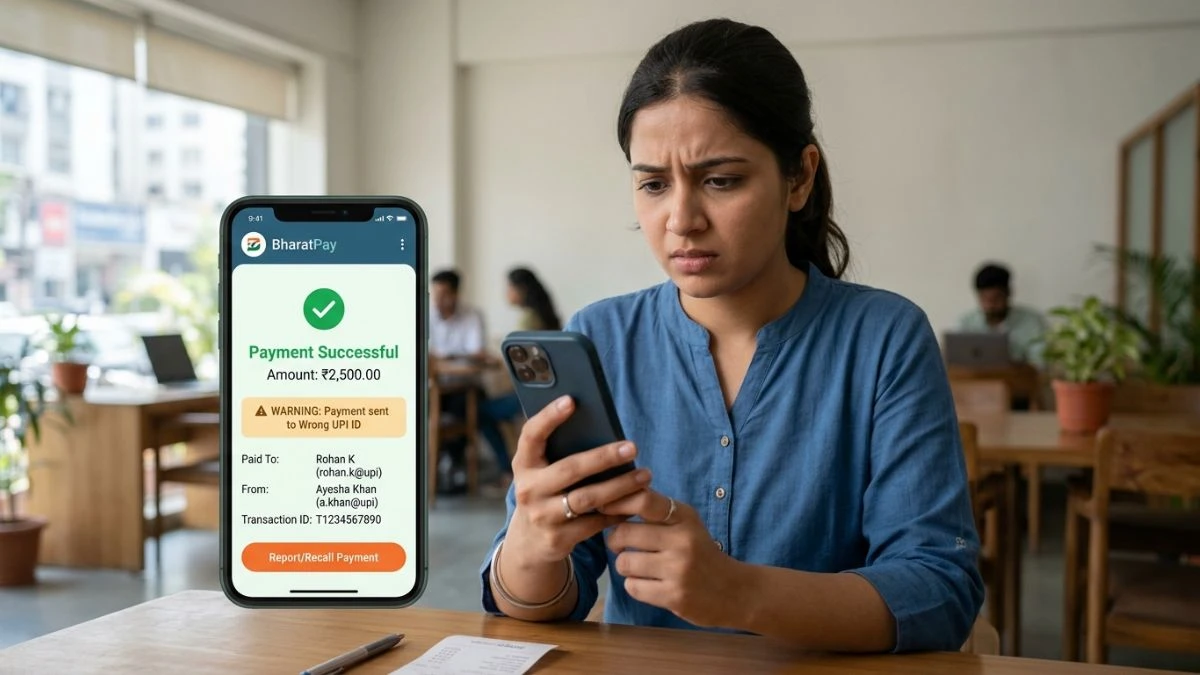

Remittance of money via UPI is now a second nature in India. It is speedy, convenient, and is popular in the country. Nevertheless, there is one severe risk associated with this convenience, as well as sending money to the wrong UPI ID.

Even a minor error when typing a UPI ID or choosing a contact may lead to the transfer of money to an incorrect account. Most users in such cases become panic-stricken and think that it is lost forever. Luckily, it is not necessarily so.

This is the guide on what will happen when you send money to the wrong UPI ID, what to do instantly and what to do to increase your chances of recovering. It is made so that it will not confuse you.

Over the last few years, as the number of digital payments in India grows exponentially, instances of inaccurate transfers have also gained presence. Most of the users, particularly the new ones to digital payments are not aware of the proper procedure of recovery. This ignorance usually results in a delay in action which decreases the possibility of refunding the money.

Knowing the right procedures, schedules, and constraints of the UPI system can prove a big difference. The timely response (within the first few minutes or even hours) may often be the difference between a successful recovery and a lost cause.

What Knowledge in a Wrong UPI Transfer

The functionality of UPI Transactions

UPI is an instant payment system that is run by the National Payments Corporation of India. After a transaction has been approved:

- The amount is debited from your bank

- It is deposited immediately in the account of the recipient.

- No automatic reversal present.

Important Reality

A successful UPI payment: unlike failed transactions, a successful UPI payment:

- Cannot be canceled

- Cannot be reversed automatically

- Relies solely on follow-up action.

It is the reason why it is essential to act fast.

The distinguishing feature of UPI as compared to other conventional banking systems is that it is real-time. In the previous systems such as NEFT or RTGS, there was occasionally a window to final settlement. The settlement in UPI occurs nearly instantly, which not only removes any delay but also erases the chance of halting a transaction after it is verified.

Moreover, UPI does not involve the use of detailed bank account numbers and hence it is easy to work with but at the cost of a possibility of human error. It is only a small mistake in typing a UPI ID which will send money to another person without any notice.

Usually, the most used methods of sending money to the wrong UPI ID include

Knowing the causes of errors will aid you in preventing future errors.

This issue may be addressed by improving the typing of UPI ID

A minor mistake can lead to the redirection of funds to another user. UPI IDs are special codes and a single wrong character may result in a legitimate but accidental receiver.

2. Choosing the Incident Wrong Contact

A lot of users are dependent on the saved contacts and end up selecting the incorrect name. This mostly occurs where there are several contacts sharing names.

3. Mixed up Like UPI IDs

Example:

rahul123@upi

rahul_123@upi

These are totally different users. The system does not authenticate intention – it just processes the ID typed in.

4. QR Code Mistakes

The wrong QR code may result in unintended transfers on scanning. This is usually done in densely populated areas or when the QR codes are exchanged online.

5. Rushing Through Payment

Majority of errors occur where the users do not verify and confirm payment in haste. The name shown as the recipient is not always checked by the users before typing in their PIN.

Multitasking is another reason that is neglected. Sometimes people pay and chat, drive or perform some other activity and this makes payment errors more likely.

Action to be taken immediately after sending money to the wrong UPI ID

Time matters. The sooner you respond the better chance of recovery.

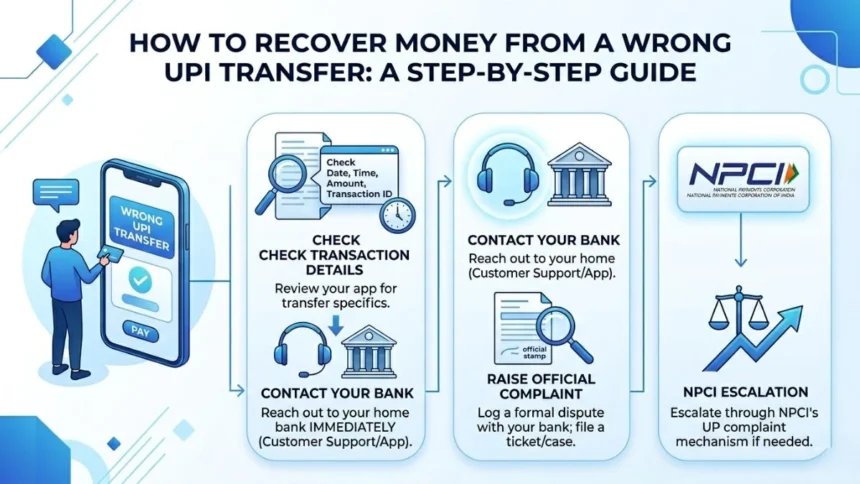

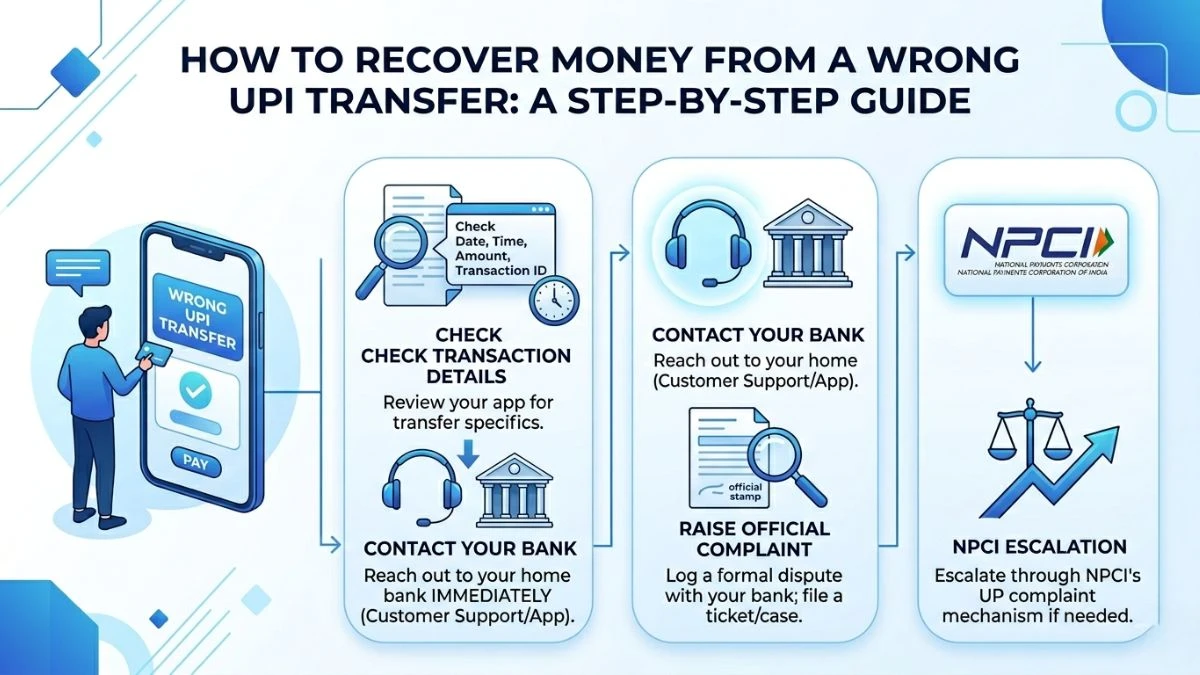

Step 1: Check the Details of the transaction

Control: Before acting, verify:

- UPI ID of recipient

- Amount transferred

- Date and time

- Transaction ID

All the subsequent steps will need this information.

One should also make a screenshot of the transaction at once. This is evidence and may be handy when submitting complaints or calling support.

Step 2: View the status of the transaction

Go to your UPI application and verify that the transaction is:

- Successful

- Pending

- Failed

In case of a pending transaction

It is still possible that it can fail or reverse on its own.

In case of a successful transaction

You need to initiate recovery measures.

Do not think that failure is a delay in confirmation. In other cases, the transactions can take a few seconds more to complete and it is best to always verify the final status.

Step 3: Communicate with the Recipient (Where possible)

In others, the name or part of the name of the recipient can be seen.

What you can do:

- Courteously ask to be refunded.

- Provide evidence of expenditure.

- Be clear in explaining the mistake.

Reality Check:

This can only be effective when the recipient cooperates. No guarantee.

In most real world situations, recipients will send the money back when made to know so. A calm and respectful tone is more likely to make you successful.

Step 4: Submit Complaint in Your UPI App

All UPI apps provide a complaint option.

Steps:

- Click on transaction history.

- Select the incorrect transaction

- Click on Report Issue or Raise Complaint.

Choose options like:

- Remitted funds to inappropriate UPI ID.

- “Incorrect transfer”

This will make sure that your problem is registered in the system.

Step 5: Call Your Bank now

Your bank is the key supporting figure.

Provide:

- Transaction ID

- Amount

- Date and time

- Screenshot (if available)

What the bank does:

- Logs your complaint

- Make contact with the bank of the recipient.

- Initiates recovery request

Banks can delay in response, but early reporting enhances the likelihood of action.

Step 6: Submit Complaint via NPCI

When the app and bank assistance is sluggish, intensify via the official system.

NPCI handles:

- UPI-related disputes

- Inter-bank coordination

Escalation will help guarantee that your case is handled formally, not just via simple support options.

Can You Get Your Money Back? (Honest Answer)

Yes, but on some conditions.

Recovery depends on:

1. Recipient’s Cooperation

Money can be refunded within a short time in case the receiver consents.

2. Bank Intervention

Banks may demand a reversal, but may not compel it in the absence of consent.

3. Lawsuit (Uncommon Cases)

Legal avenues might assist in case of fraud.

Recovery Becomes Difficult When

- In case of refusal by the recipient to give back money.

- In case of a wrong UPI ID of an active user.

- In case there is too much delay in reporting.

Among the largest causes of failure in recovery are the delays. The more time you take, the more difficult it is to trace and undo the transaction.

What Banks and UPI System Can (and Cannot) Do

What They Can Do

- Record your complaint

- Contact receiving bank

- Request refund

What They Cannot Do

- Automatically reverse a completed UPI transaction.

- Steal money belonging to the recipient.

This is a limitation in that UPI is a secure system in which users authorize transactions.

What is the Duration of The Recovery Process?

Recovery timelines vary:

- Immediate (assuming that the recipient agrees)

- Few days (bank follow-up)

- Weeks (unless escalation necessary)

It is also important to be patient but follow-up regularly.

Legal Options in Case of Non-Cooperation

In case the recipient refuses repaying money:

You can:

- Bank complaint.

- Report using a cyber crime portal.

- Approach local authorities

Only in high-value cases, legal action is generally taken into consideration.

The UPI Safety Rules to Be Observed

It is much more effective to prevent than to cure.

Always Check Recipient Name

Before confirming payment:

- Check displayed name

- Make sure it corresponds with the intended recipient.

2. first send a Little Test Quantity

For new transactions:

- Send ₹1 or small amount

- Confirm recipient

- then send full amount

3. Avoid Rushing Transactions

Allow extra few seconds to:

- Verify UPI ID

- Confirm details

4. Auto-Save Verified Contacts

Do not save the unknown or unverified UPI IDs.

5. Double-Check QR Codes

Make sure that QR code is of the right person or company.

Let’s Take An Example:

Imagine:

You wanted to remit ₹5,000 to a friend.

Rather, you entered another UPI ID and transferred money to a different individual.

What happens next:

- Money is instantly credited

- No automatic reversal

- You have to start the healing process yourself.

Best outcome:

Recipient returns money

Worst case:

Recovery becomes difficult

Such scenarios underscore the need to be careful to verify any payment.

More Read

Failed Transaction vs. Wrong Transfer

Many users become confused here.

| Situation |

Refund |

| Payment failed | Automatic refund |

| Wrong UPI transfer | Manual recovery needed |

Frequently Asked Questions

1. Is it possible to reverse a UPI transaction once the money is sent?

No, once it is processed, it is not cancelable.

2. Does the bank automatically reverse the transaction?

No, banks cannot demand a reversal, they can only request.

3. What do I need to do initially after a wrong transfer?

Immediately report the issue in your app and contact your bank.

4. Can money be recovered without cooperation of recipients?

Hard, and could be done, however, by legal or banking escalation.

5. What can I do to prevent such errors in the future?

Confirm information and remit a small amount.

Conclusion

One of the most serious yet frequent mistakes is to send money to a wrong UPI ID. Although the system does not provide automatic reversals, the sooner you withdraw, the better shot you have of recovery.

The key is to:

- Act immediately

- Use official channels

- Remain patient and do the right thing.

UPI is a very strong mechanism, but, as any financial mechanism, it must be used with care. You can save hours of stress by a few additional seconds of verification.

About The Vue Times

The Vue Times is an online platform that aims at making complex issues in the areas of technology, finance, public policy and daily matters in India easier. Our goal is to present clear, practical and research based information that enables the readers to understand real-life issues and make good choices.

Editorial Note

The editorial team at The Vue Times has reviewed and checked this article to ensure that it is accurate, clear and usable in practice. The data is informed by publicly available data, formal guidelines and real-world user scenarios in India.

Disclaimer

The article should be informative in nature. Although all attempts have been made to be precise, policies, banking operations as well as regulations can change with time. It is recommended that the readers should confirm information with the official sources or the bank they belong to and then do whatever they deem necessary.